“Identity will be the most valuable commodity for citizens in the future, and it will exist primarily online.”― Eric Schmidt

As digital technologies advance and most facets of our lives get gradually digitalized, we will get to the point where our primary identity will be established – and then maintained- in the online realm. Will this “identity revolution” affect the financial industry? Well, it already does. Since most transactions and interactions already happen online, building digital trust and investing heavily in safeguarding customers’ identities has turned into a top priority for all financial institutions. Boasting a robust financial system and a booming tech industry, Germany is no exception to this global trend. Will the German financial industry be able to seize the underlying opportunities and mitigate risks? In today’s article, we will take a look at how Germany is implementing digital identity verification in the financial sector. Elinext’s article on fintech for retirement processes examines how digital platforms are being applied to pension fund management, retirement savings automation, and annuity administration — covering the regulatory compliance requirements, integration patterns with payroll and banking systems, and the user-facing features that help employees track and manage their retirement contributions.

What is digital identity verification?

Widely used in industries such as finance, healthcare, telecom, or e-commerce, digital identity verification involves the use of technological solutions to authenticate the identity of a person or entity during online interactions and transactions. Digital identity verification solutions – such as biometric verification, AI-powered data analysis, two-factor and multi-factor authentication, blockchain, document verification, or knowledge-based verification – typically involve the collection of personal data whose authenticity is afterwards confirmed by cross-referencing it with public records, existing databases, or other third-party sources.

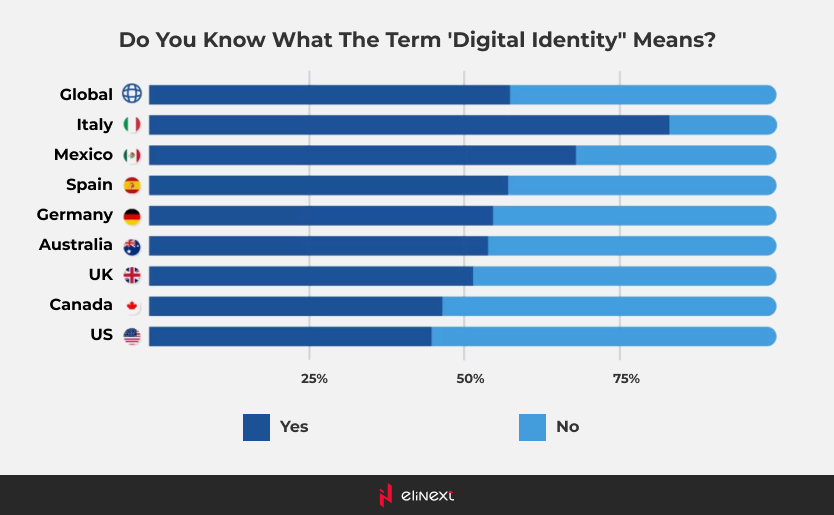

Using digital identity verification not only has significantly reduced the risk of identity theft, fraud, and unauthorized access to sensitive data but has also increased customers’ trust in online operations. However, the concept of digital identity is still causing confusion among consumers. As a result of the survey carried out in 2022 in which participated 16,000 consumers from 8 countries, iProov found that 42% of the global consumers do not know what digital identity means.

When digging deeper into the respondents’ understanding of digital identity, 52% of the German respondents were the closest to the truth, opting for ‘any information that exists about me online’.

Which is the bottom line? The implementation of digital identity verification can only be successful if it focuses on customer education. Helping customers fully understand all the benefits and all the processes involved is the only way to enhance the acceptance of digital identity verification.

Digital Identity Verification: Market Size, Opportunities, and Risks

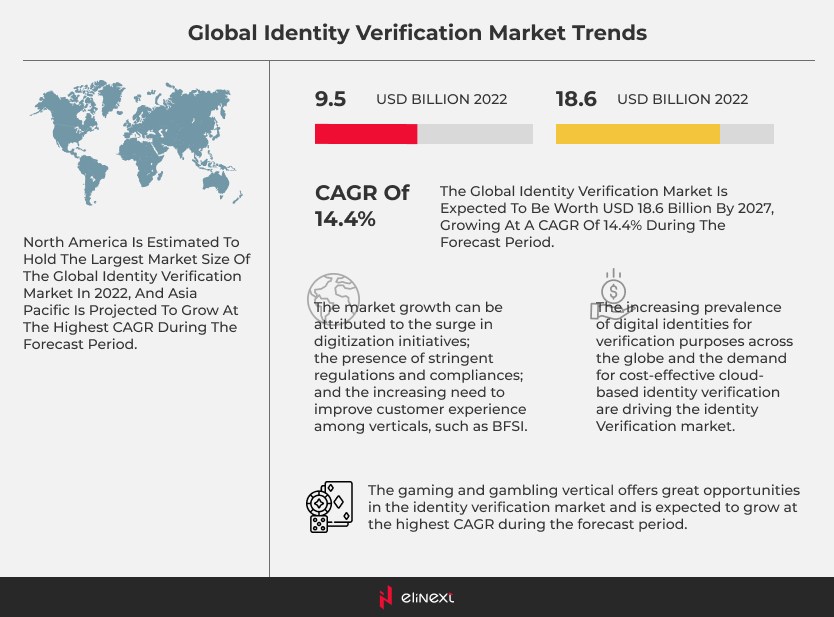

According to MarketsandMarkets, in 2022, the global identity verification market was valued at $9.5 billion and it is expected to grow at a CAGR of 14.4%, reaching $18.6 billion by 2027.

According to the same report, this is how the market ecosystem looks like:

Which are the main opportunities for financial institutions?

Undoubtedly, our physical and digital worlds are increasingly more connected. Investing in digital identity verification can unlock a series of opportunities. Let’s take a look at some of them:

Frictionless and user-friendly customer experiences

The use of innovative technologies such as biometrics, blockchain, or AI, can streamline processes, allows customers to securely and conveniently make transactions, open accounts, or apply for a loan remotely.

Reduced processing times and operational costs

Relying on automated systems not only translates into fast customer identity authentication but also into quick risk assessments and document validation, thus reducing costs and improving operational efficiency.

Improved personal data protection and fraud prevention

The use of emerging technologies such as biometrics or AI as a replacement for traditional passwords or usernames, adds an extra layer of security, thus enhancing customers’ trust. What’s more, advanced algorithms and ML-powered solutions can identify potential fraudulent activities by analyzing huge amounts of data and detecting anomalies.

Regulatory Compliance

Digital identity verification can help financial institutions ensure compliance with all the strict regulations such as KYC or AML.

Which are the main risks?

Let’s take a look at the other side of the coin:

Data Privacy and Security Concerns

It is true that digital identity verification enhances security. But concerns about data breaches and data privacy still prevail. Protecting their customer data from cyberattacks or unauthorized access has led financial institutions to invest heavily in robust security measures, often turning to financial software solutions to safeguard sensitive information.

Technological challenges and limitations

Compatibility issues, lack of expertise, outdated IT systems, or system vulnerabilities, are only some of the challenges financial institutions need to address to successfully adopt digital identity verification.

Customer acceptance

Not all customers are tech-savvy, have access to the necessary technology, or feel comfortable using digital identity verification. To avoid exclusion, financial institutions should ensure alternative methods.

False positives

Algorithms and ML-powered solutions can fail, blocking legitimate transactions or denying access to genuine customers. Financial institutions should not only invest in refining their algorithms but should also provide solid customer support able to solve any verification issue in a timely manner.

How is the German financial industry tackling the digital identity verification challenge?

Over the past years, German financial organizations have taken multiple initiatives and approaches to efficiently address the digital identity verification trend.

Close partnership with regulatory bodies

To ensure compliance with all the pertinent regulations related to digital identity verification, German financial institutions collaborate closely with BaFin (Federal Financial Supervisory Authority) and BfDI (Data Protection Authority) to establish a standardized framework for identity verification processes and ensure customer data protection.

Use of biometrics

Many German financial institutions are already using biometrics in their digital identity verification processes. The use of biometric authentication methods – such as fingerprints, facial or voice recognition, or behavioral biometrics – has increased the level of security and accuracy in customer identity verification, thus reducing the risk of identity theft and fraud.

For instance, Deutsche Bank, one of the largest banks in Germany, has implemented biometric authentication for its mobile banking app. Customers can use fingerprints, facial recognition, or behavioral attributes to securely log in to their accounts and authorize transactions. Similarly, other prominent German banks such as Commerzbank, N26, DKB, or Postbank, have incorporated biometric technology into their digital services, thus enhancing security and providing their customers with a seamless and user-friendly authentication experience.

Implementation of blockchain technology

This innovative decentralized ledger system is already revolutionizing the financial sector, offering outstanding benefits such as enhanced security, transparency, operational efficiency, and enhanced customer experience. German financial institutions such as Deutsche Bank or Commerzbank are already investing in multiple blockchain projects (e.g. Project DAMA or Commerzbank’s blockchain-based payment test) focusing on areas such as cross-border payments, cryptocurrency, digital funds administration, or identity verification.

Close partnership with FinTech startups

German financial institutions are well-known for collaborating closely with innovative FinTech startups to diversify their services, streamline processes, enhance customer experience, and – above all- stay at the forefront of digital innovation. One excellent example could be the collaboration between IDnow and Commerzbank. This partnership simplified the onboarding process. The integration of IDnow’s video identification technology into Commerzbank’s digital platform allows customers to securely and conveniently verify their identities remotely. And examples could continue: Verimi and DZ Bank, Authada and Sparkassen, or IDnow and HypoVereinsbank.

But collaboration with Fintech startups goes well beyond digital identity verification. For instance, Deposit Solutions and Deutsche Bank launched the ZINSmarkt platform, allowing customers to access deposit products from other banks via a single interface. Another example could be the collaboration between Elinext and another German digital banking company for the development of a customized invoice automation system.

Collaboration with a trustworthy network of service providers

To ensure compliance with the eIDAS regulation when providing secure digital identity solutions, German institutions collaborate closely with trusted service providers such as Bundesdruckerei, Deutsche Telekom, D-TRUST, or DATEV.

Wrapping up

Digitalization is taking us all by storm. And the financial industry could be no exception. The use of innovative technologies – such as biometrics, blockchain, or AI-powered solutions – for digital identity represents a double-edged sword for financial institutions. On the bright side we find opportunities such as streamlined processes, enhanced security measures, improved customer experiences, operational efficiency, cost reduction, and competitiveness. But it is impossible not to take into consideration as well concerns about data privacy, technological limitations, lack of expertise, or user acceptance. However, the German financial industry is actively tackling all these challenges and opportunities.

About the Author

Anastasia is a financial and banking IT consultant at Elinext with over 10 years of experience in fintech project delivery. She specializes in client management, RFP bidding, and cross-functional coordination for complex financial sector solutions — helping businesses bridge the gap between regulatory requirements and scalable software implementation.