In 2025, blockchain solutions for businesses are transforming industries by offering secure, transparent, and automated processes. The global blockchain market is projected to reach $94 billion, with 90% of businesses implementing blockchain development solutions. Key trends include modular blockchain architecture, zero-knowledge proofs for privacy, and tokenization of real-world assets. Supply chains use blockchain for real-time tracking, while financial institutions use it for instant settlements and compliance. Companies are seeing increased efficiency, reduced fraud, and new revenue streams from blockchain for business.

What are the Blockchain Solutions for Business

A logistics company uses blockchain to trace shipments in real time, reducing fraud and paperwork. Financial firms automate settlements and compliance, while retailers use blockchain for loyalty programs and anti-counterfeiting. These solutions deliver transparency, automation, and cost savings across sectors. Blockchain solutions for business include smart contracts, digital identity, supply chain tracking, secure payments, and decentralized cloud storage.

Building Trust and New Business Models

- The power of ecosystem to manage processes in a faster manner

- The absolute transparency of deals

- The creation of cost-efficient decentralized business networks

- The ability to create trusted partnerships and new business models

Key Takeaways

- The global blockchain market is projected to reach $94 billion in 2025

- 90% of enterprises are using or planning to use blockchain solutions

- Asset tokenization is expected to reach $16.1 trillion by 2030

Blockchain Solutions for Business by Elinext

Blockchain solutions for business from Elinext, combined with financial software development services, create comprehensive platforms for payments, compliance, and asset management. Elinext helped a bank implement a blockchain-based KYC system, reducing customer onboarding time by 60%. Elinext’s solutions automate settlements, enhance security, and ensure compliance, increasing efficiency and customer confidence in financial transactions.

-

Smart Contracts Solutions

An insurance company uses smart contracts to automatically approve claims when conditions are met, reducing processing time and eliminating manual errors. This increases efficiency and trust between parties. Blockchain business opportunities include smart contracts that automate agreements and transactions.

-

Salaries and Money Transfers

Blockchain for business streamlines payroll and remittances with instant and low-cost transactions. A multinational company pays remote employees in different countries using blockchain, reducing transfer fees and settlement times from days to minutes, while ensuring transparency and security.

-

Cyber Security Solutions

Blockchain improves cybersecurity by providing secure records and decentralized authentication. A healthcare provider secures patient data on the blockchain, preventing unauthorized access and reducing data breaches while ensuring compliance with privacy regulations.

-

Loyalty Programs

Blockchain for business enables transparent, fraud-proof loyalty programs. A retailer issues rewards points on the blockchain, allowing customers to instantly redeem or transfer them. This increases engagement and reduces the risk of double spending or fraud.

-

Cloud Storage Solutions

Blockchain-based cloud storage distributes data across a decentralized network, improving security and uptime. A media company stores digital assets on a blockchain platform, ensuring that files are protected from unauthorized access and accessible even if one of the servers fails.

-

Electronic Voting

Blockchain for Business enables secure and transparent electronic voting. A city administration uses blockchain to record votes in local elections, ensuring protection from unauthorized access and the ability to audit results, which increases public trust in the electoral process.

-

Blockchain Business Consulting Solutions

Blockchain business consulting helps companies develop and implement blockchain strategies. A consulting firm is helping a manufacturer implement blockchain to provide supply chain transparency, resulting in faster product recalls and increased compliance with industry standards.

Unlock efficiency and security—order custom blockchain solutions for business today!

Secure the future of your company with Elinext blockchain development solutions tailored to the needs of your industry.

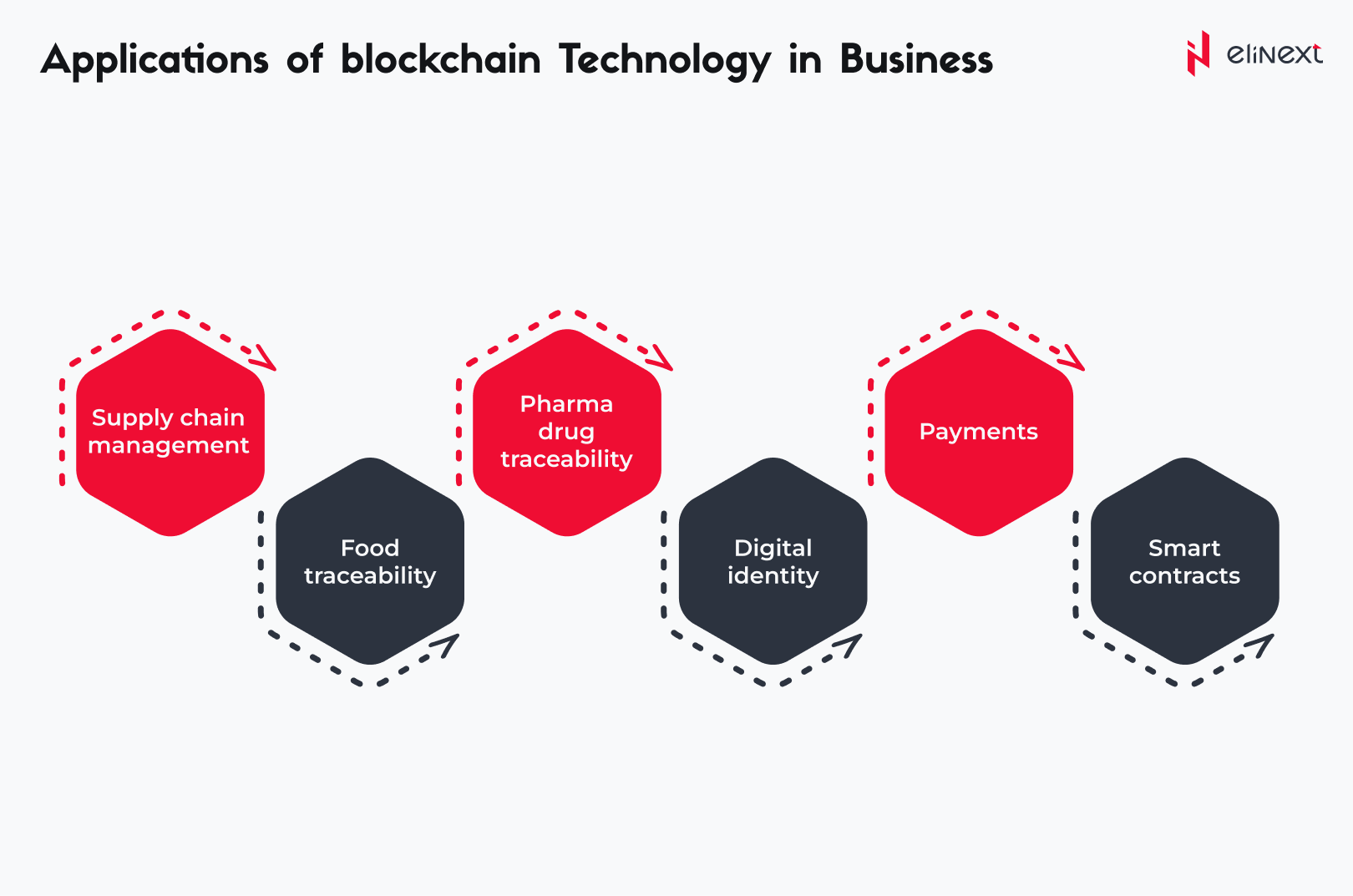

Blockchain for Business in Different Industries

Blockchain solutions for business are used in finance (payments, KYC), healthcare (patient data), supply chain (tracking), and government (voting). Walmart uses blockchain to track the origin of food products, reducing response times from days to seconds.

-

Supply Chain Management Solutions

Blockchain business opportunities in supply chain management include real-time tracking and fraud prevention. Maersk’s TradeLens platform uses blockchain to digitize shipping documents, reducing paperwork and speeding up customs clearance, saving millions of dollars annually.

-

Pharma Drug Traceability Solutions

Blockchain enables traceability of drugs from the manufacturer to the pharmacy. Pharmaceutical companies use blockchain to track each batch, preventing counterfeiting and ensuring compliance. This improves patient safety and simplifies regulatory reporting. Pharma drug traceability with finance software development services: secure ledgers, audits, and recalls.

-

Payments Solutions

Blockchain solutions for business enable instant payments with low fees. JPMorgan’s Onyx platform uses blockchain for interbank transfers, reducing settlement times from days to minutes and reducing transaction costs while increasing accountability.

-

Food Traceability Solutions

Blockchain tracks food from farm to table. Walmart’s blockchain system traces pork in China, reducing the time to identify contamination sources from days to seconds, improving food safety and consumer trust. Food traceability powered by finance crm software development: track batches, audits, recalls, and supplier compliance.

-

Digital Identity Solutions

Blockchain solutions for business provide secure digital identity management. Banks use blockchain to verify customer identities, reducing onboarding time and preventing identity fraud, while allowing users to control their personal data.

What are the Future of Blockchain Solutions for Business

The future of blockchain solutions for business is defined by modular architectures, privacy technologies, and asset tokenization. By 2030, blockchain is expected to create $16.1 trillion in business value and 40 million jobs. Businesses will leverage blockchain for AI integration, green initiatives, and interoperability across networks. Tokenized assets and decentralized identity will become standard, while regulatory clarity and sustainability drive further adoption and innovation

“Blockchain business consulting opens up new opportunities for enterprises. We help clients automate processes, protect data, and build trust. For example, our blockchain solutions optimize supply chains and payments, delivering measurable ROI and a future-ready infrastructure.”

Elinext Blockchain Expert

Conclusion

Financial CRM software development and blockchain for business are combining to create secure, automated, and transparent solutions. In 2025, blockchain will be the foundation of payments, supply chains, digital identity, and compliance across all industries. Banks use blockchain for instant settlements, while retailers track goods in real time. With a projected market size of $94 billion and 90% adoption in companies, blockchain plays a key role in driving efficiency, trust, and innovation. Partner with experts to help your business leverage these trends for sustainable growth.

FAQ

- What is blockchain for business?

Blockchain for business is a secure, decentralized technology that automates and records transactions. Companies use blockchain to track goods, process payments, and manage contracts, increasing transparency and reducing the risk of fraud.

- How does blockchain improve business processes?

Blockchain streamlines business processes by automating transactions, reducing paperwork, and ensuring data integrity. Smart contracts ensure that agreements are automatically executed, and supply chains use blockchain for real-time tracking and fraud prevention.

- What are the key blockchain solutions for businesses?

Key blockchain solutions include smart contracts, digital identity, supply chain tracking, secure payments, and decentralized storage. Banks use blockchain for instant payments, and retailers use it for loyalty programs and anti-counterfeiting.

- What industries benefit most from blockchain?

Finance, supply chain, healthcare, government, and retail are the industries that benefit the most from blockchain. Banks use it for payments, pharmaceuticals use it to track medicines, and governments use it for secure voting and digital identity management.

- Is blockchain cost-efficient for businesses?

Yes, blockchain reduces costs by automating processes and eliminating intermediaries. Cross-border payments on blockchain are faster and cheaper than traditional methods, saving companies time and reducing transaction fees.