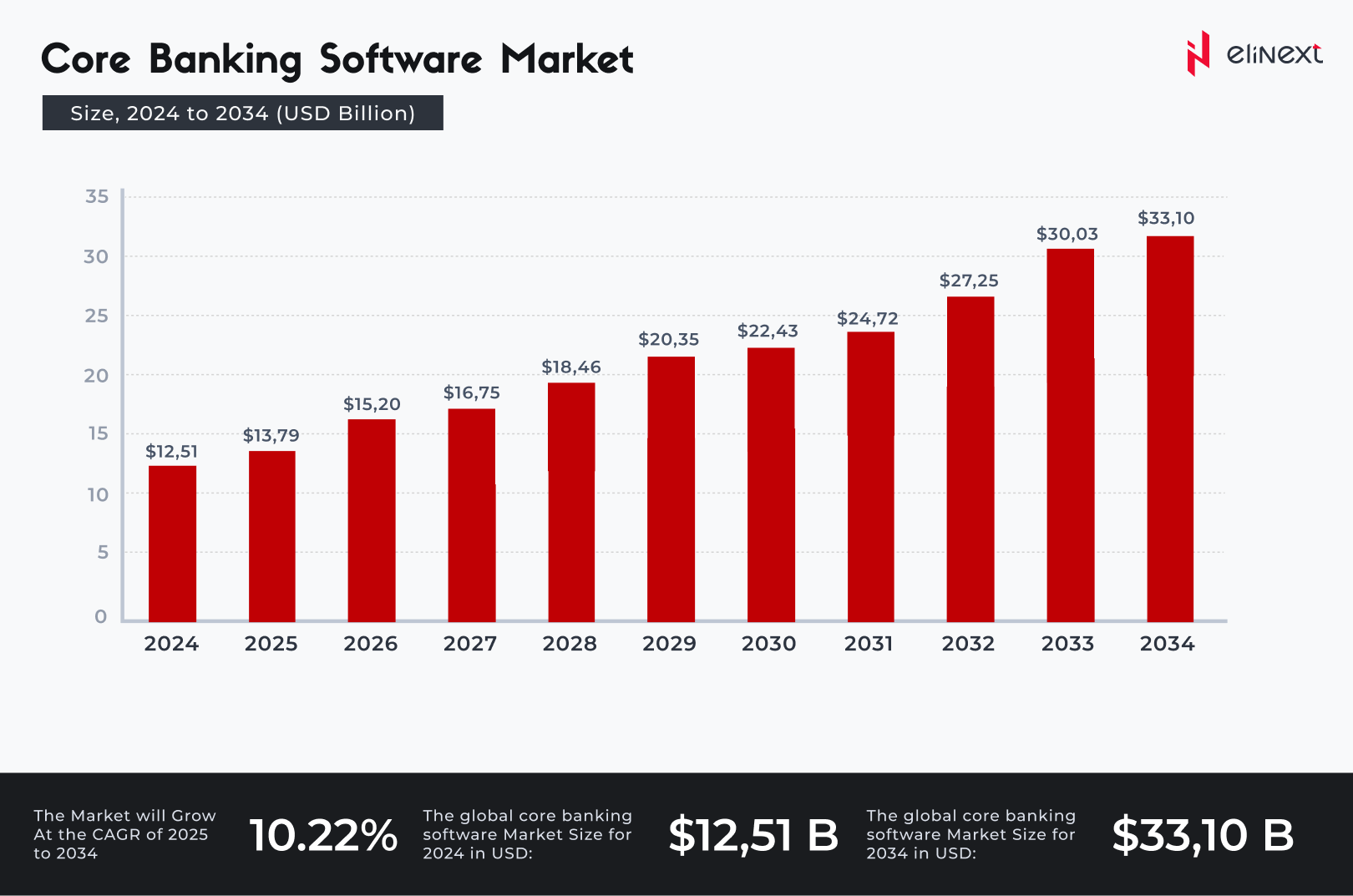

In 2025, banking software development trends will be driven by cloud platforms, AI-powered analytics, and real-time payments. Banking software development solutions focus on open banking APIs, cybersecurity, and embedded financial solutions. 92% of European banks now use AI for fraud detection, and digital onboarding reduces customer onboarding time by 45%. Analytics show that banks implementing these trends see a 38% increase in customer satisfaction and a 31% reduction in operating costs.

Top Banking Software Engineering Solutions in the Europe Market

-

Digital Banking

Banking customers are no longer required to be physically present or on-site to successfully conduct any financial transaction. Digital banking evolves with software engineering banking trends 2025: AI personalization, instant payments, open APIs, zero-trust security, and cloud-native cores driving speed and scale. The rise of digital banking services like virtual assistants, online banking portals, and mobile banking app solutions retain such customers from a remote comfort zone while meeting their financial needs on vetted cloud computing platforms.

-

Mobile Payments

Mobile payments surge with software engineering trends in banking: tokenization, instant rails, and biometric UX. Consumers with smartphones continue to flexibly adapt to the comfort of making payments via mobile devices. Smartphone companies are also on a competitive quest of producing smartphone gadgets with integrated, secure, and reliable payment systems like Samsung Pay, Apple Pay, and Google Pay to lessen user banking hurdles.

-

Sustainable Finance

Sustainable finance advances with banking software engineering trends: ESG data pipelines, impact scoring, and green loan tracking. The yearly carbon footprint associated with the manufacturing, processing, and distribution of banking cards like Visa and Mastercard have a significant impact on global warming and climate change. In order to target and retain customers that are conscious about a low-carbon economy, most banks are digitizing their products and services to promote an environment-friendly banking environment for their customers.

-

Blockchain Technology

The benefits of blockchain in the banking industry are straightforward because every transaction is recorded and validated, third-party authorization is not a mandate, and the technology is decentralized. Blockchain development solutions power secure, transparent ledgers, smart contracts, tokenization, and cross-border settlements. Bank blockchains beat traditional banking systems in terms of speed and affordability when handling cross-border payments. In trading transactions, information redundancy is reduced in favor of performance.

-

Open Banking

Application Programming Interfaces (APIs) make it possible for third-party fintech (financial technology) companies and banking bodies to share user financial data like bank statements and transaction patterns, hence the concept of open banking. The use of third-party fintech companies gifts consumers security and flexibility in their financial management routines. Open Banking thrives with finance software development services: secure APIs, consent flows, data sharing, and fintech integrations.

-

Biometric Technology

Biometric tech, aligned with software engineering trends in banking: face/voice ID, liveness checks, and passive fraud detection. Biometric technologies support fingerprints and facial recognition features to uniquely identify banking customers. This technology makes it complicated for hackers to remotely access and steal/compromise banking customers’ financial data. Therefore, this dominant financial software trend adds an important security layer for customers vulnerable to weak user passwords that can be compromised via prominent account hacking techniques like dictionary attacks.

-

Cybersecurity

Common Cybersecurity threats include the implementation of ransomware and social engineering attacks. With ransomware, an organization is locked out of its system with the demand of ransom for system re-access (which is not guaranteed). Cybersecurity powered by data analytics services: detect anomalies, predict threats, prioritize risks, and automate response.

Most banks have opted to partner with Cybersecurity companies with dedicated security software and intrusion detection systems to help deal with such Cybersecurity threats. Also, the implementation of security and consumer awareness training programs helps lessen the prominence of social engineering attacks.

-

VR / AR Solutions

The use of AR and VR in training and recruiting banking staff is a flexibly empowering move in the financial sector. VR/AR solutions powered by AR/VR app development services: immersive tours, training sims, 3D design, and remote assist. VR technology promotes the concept of virtual banks with virtual branches for seamless offsite execution of banking activities. Both technologies save data analysts from navigating through multiple screens to make sense of user data.

-

Big Data and Analytics

Big Data and Analytics, driven by banking software engineering trends: real-time risk scoring, personalization, and fraud detection. Big data and analytics output helps the sales and marketing teams create demographic campaigns and identify potential long-term customers. Big data development services also paint a clear picture of potential consumer challenges and their resolution. This technology is also useful in fraud detection and prevention via the periodic analysis of consumer behavior and transactional data patterns.

-

Robotics Process Automation (RPA)

Automatic ticketing systems have solved the traditional queuing approach of serving clients, which in some instances led to overcrowding and overwhelmed banking customers. Presently, most banking customers are assigned a ticket number via RPA on their visit to the bank and are promptly alerted and guided on which area of the bank they will receive the needed financial aid. Humans with data entry and document processing skill sets that previously undertook these roles lacked the efficiency, accuracy, and speed of RPA.

-

AI and ML Solutions

AI and ML solutions, via artificial intelligence development solutions: predictive insights, automation, personalization, and risk scoring. European banks are making use of AI-powered Chatbots for faster responses to user queries. The evolution of these Chatbots enables them to recognize customers’ emotions and respond with the needed emotional sensitivity. AI and ML collaboration has simplified online banking. It is now easier for banks to pull information from uploaded documents, hence the reason why smartphones are now convenient for uploading and depositing bank checks.

Unlock the potential for efficiency and innovation — order custom banking software development from Elinext! Teams building financial planning tools can reference Elinext’s overview of fintech for retirement processes, which outlines the product design considerations for retirement-focused fintech — from automated contribution management and projection tools to the compliance requirements that govern the handling of long-term savings data in regulated markets.

Modernize your systems with AI, cloud technology, and secure solutions designed for the future of banking.

What is the Future of Banking Software in Europe

Software engineering banking trends 2025 predict a surge in AI adoption, blockchain-based transactions, and hyper-personalized banking apps. European banks are embracing digital ecosystems with built-in financial systems and instant payments. For example, fintech partnerships allow banks to launch super apps for complex financial services, increasing customer retention and increasing revenue sources. Analytics show that banks that invest in cloud development reduce IT costs by 27% and implement new features 3 times faster, remaining leaders in a competitive market.

“Key trends in banking software development are being driven by AI, cloud applications, and open banking APIs. Our solutions provide banks with real-time analytics, enhanced security, and a seamless digital experience. Clients report up to 38% increase in customer satisfaction and rapid development of innovative products.”

Elinext Software Development Expert

Conclusion

Finance CRM software development and banking engineering trends are now focused on security, real-time data, and a seamless digital experience. In 2025, banks will use AI for fraud prevention, cloud for scalability, and open APIs to integrate fintech solutions. Banks with embedded financial platforms are seeing a 31% increase in cross-selling and a 27% decrease in IT costs. Implementing these trends allows banks to remain competitive, compliant and prepared for rapid innovation in the digital age.

FAQ

What are the main software trends in banking today?

Software engineering banking trends 2025 highlight AI-powered risk analytics, cloud applications, and open banking APIs. Banks are using AI to detect fraud, and cloud solutions to launch new digital products faster and more securely.

Why is cloud technology important for banks?

Banking software engineering trends show that cloud and AI are improving security, agility, and analytics. Cloud platforms enable rapid scaling, while AI analyzes transactions in real-time to combat fraud and personalize customer service.

How is AI changing banking software?

AI is transforming apps with fraud detection, chatbots, and hyper-personalized offers. AI flags anomalous card activity in milliseconds and advises next-best actions—core to banking software engineering trends.

What role does blockchain play in banking?

Blockchain has enabled secure, verifiable transfers and tokenized assets. Example: banks use blockchain for instant cross-border settlements, reflecting software engineering trends in banking.

What is open banking and why does it matter?

Open banking allows customers to share data through secure APIs to access better services. Example: A budgeting app that combines accounts and offers personalized loans is a key in banking software engineering trends.

How are banks improving cybersecurity?

Banks are implementing zero trust, multi-factor authentication (MFA), AI threat hunting, and confidential computing. Example: Real-time anomaly detection prevents account theft — hallmarks of banking software engineering trends.

About the Author

Anastasia is a financial and banking IT consultant at Elinext with over 10 years of experience in fintech project delivery. She specializes in client management, RFP bidding, and cross-functional coordination for complex financial sector solutions — helping businesses bridge the gap between regulatory requirements and scalable software implementation.