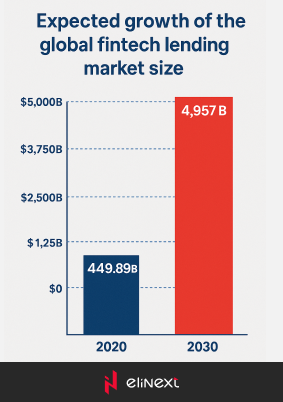

The global fintech lending market size was capped at a whopping $449.89 billion. More to that, by 2030 this sector of the financial market is expected to be valued at $4,957 billion with an impressive annual growth rate of 27.4%.

According to Allied Market Research, that is connected with a surge of new-wave fintech companies. Fintech adoption rates are growing around the world. 64 percent of global financial consumers use FinTech. One of the biggest markets in Europe is Germany. The German fintech is second-ranked in Europe with raised investments to the market of over EUR 2.1 billion. Alternative lending has emerged as a major disruptor in the German credit market.

So in this blog post, we’ll explore how fintech is changing the German credit market and what it means for the future of lending.

What is Alternative Lending?

In Germany, alternative lending refers to the provision of loans to individuals and businesses through unconventional means, typically facilitated by online platforms and fintech companies.

Typically, alternative lending platforms utilize technology to connect borrowers with investors or lenders, streamlining the process of obtaining credit and making it more convenient.

Moreover, these platforms frequently provide more adaptable loan terms and lower interest rates compared to conventional banks.

Due to stricter regulations and heightened capital requirements imposed on traditional banks, their willingness and ability to grant loans have diminished. Usually, alternative lending platforms use technology to connect borrowers with investors or lenders, making it easier and faster to access credit. They also often offer more flexible lending terms and lower interest rates than traditional banks. The European Commission in many ways encourages the increase in non-bank lending. Their effort is paired with an increase in companies seeking alternative forms of finance to loans.

This is one of the priorities of the Capital Markets Union (CMU) initiative. To achieve this goal, a set of initiatives is being pursued, which includes encouraging fund-based loan origination and facilitating investments in venture capital, infrastructure, and equity.

Alternative Le ding Variations in the German Credit Market

Germany has traditionally been a market dominated by traditional banks. However, in recent years, fintechs have made significant inroads into the credit market. PwC reports that Germany is the third-largest fintech market in Europe: more than 800 fintech companies are operating in the country. There are numerous listings with companies worthy of checking out on the market.

Peer-to-Peer for individuals

One area where fintechs have made a significant impact is in the peer-to-peer lending space. Peer-to-peer lending platforms like Auxmoney and Smava have grown rapidly in recent years, offering borrowers an alternative to traditional bank loans. These platforms use AI algorithms to match borrowers with individual investors, allowing borrowers to access credit quickly and easily.

Peer-to-Peer for businesses

Peer-to-peer business lending is also a thing quite popular among SMEs in Germany. Anyone really can invest in particular companies looking for a loan. One can use marketplaces with minimal investments as small as €50.

Other types of alternative lending

Crowdfunding has also become a popular alternative lending option in Germany.

Platforms like Seedmatch allow entrepreneurs to raise capital from a large number of investors without having to go through the traditional fundraising process.

This has made it easier for small businesses to access funding, which can be a challenge in a market dominated by traditional banks.

Marketplaces

We should highlight that marketplace lending platforms act as intermediaries, connecting borrowers with multiple lenders. Among the popular marketplace lending platforms in Germany are Creditshelf, and Lendico. Elinext’s breakdown of netflix dominates the market is apple plus a threat analyses the subscription model economics and content investment strategies driving competition in the streaming sector — useful context for product teams designing media applications or evaluating the feature bar set by established platforms.

If you’re looking for a reliable and experienced software development partner, check out Elinext’s portfolio in the financial domain. We help companies in Germany and beyond by delivering top-notch custom financial software.

Impact on the German Credit Market

Why are investors so interested in entering the market of lending platforms?

Constantin Fabricius, Managing Director of the Association of German Lending Platforms in his recent interview answered this one. He said that with low-interest rates (as on the market right now) it is very difficult to find a way to profitably invest money and find risk-worthy opportunities.

People are starting to look for options outside of mezzanine forums, retail, and institutional investors managed to come to the conclusion that lending platforms can offer good performance and deliver attractive yields.

“Investing via marketplace lenders remains an option for investors’ portfolios, as the performance offers expected return potential as well as added value in the asset mix due to low correlation with other asset classes”, – Fabricius added.

One of the biggest benefits of alternative lending is that it has increased competition in the market. This has led to more choices for borrowers and lower interest rates.

Risks and Downsides of Alternative Lending

One concern is that it could lead to increased risk in the financial system.

Fintechs are not subject to the same regulatory oversight as traditional banks, which could lead to a lack of accountability in the event of a financial crisis. However, there are some regulations (not as conservative as for traditional banks, but still).

So there is work in that direction. After all, fintech lending platforms are required to comply with various laws and regulations, such as the German Banking Act, and the German Securities Prospectus Act. Additionally, some worry that the algorithms used by fintech to assess creditworthiness could perpetuate existing biases in the credit market.

Obviously, there could not be perfect algorithms, but AI is really helpful in creating one. Scaling mire it would be possible to witness significant growth in the use of blockchain technology for lending. Blockchain has the potential to revolutionize the lending process by offering a more secure and transparent way of recording transactions.

It could also make it easier for borrowers to access credit without having to go through a middleman, such as a bank or lending platform.

Another area of potential growth is in the use of Artificial Intelligence and Machine Learning to assess creditworthiness. Market-dominating fintechs are already using algorithms to assess credit risk, but as technology continues to advance, we can expect these algorithms to become even more effective. These algorithms will give the opportunity to get potential customers among those who might have been excluded from the traditional banking system.

Conclusion

Alternative lending is changing the German credit market in significant ways. Fintechs have introduced greater competition, more flexibility, and lower interest rates to the market due to better regulation conditions. Credit becomes more accessible to those who struggle to get one from the traditional banking system, which has certain backdraws, but also opens extra opportunities.

While there are concerns about potential risks associated with alternative lending, the future of the industry looks bright and profitable. As technology continues to advance, we can expect to see even more innovation in the alternative lending space, which could transform the way we borrow, lend, and invest in the years to come.

Elinext could serve as a software development partner that could help you in creating groundbreaking lending tools on the German market. Contact us for a free quote. It seems like a challenge for German lending startups. Requirements for scaling and expanding internationally are crucial for fintech companies in Europe. It is essential for international companies to overcome barriers presented by variations in languages, regulations, cultures, and even currencies, even within the European Union, in order to successfully grow their operations.

About the Author

Anastasia is a financial and banking IT consultant at Elinext with over 10 years of experience in fintech project delivery. She specializes in client management, RFP bidding, and cross-functional coordination for complex financial sector solutions — helping businesses bridge the gap between regulatory requirements and scalable software implementation.