Virtual healthcare solutions integrate telemedicine, remote monitoring, and mHealth into a single digital ecosystem. Telemedicine is a broader concept encompassing both clinical and non-clinical remote services, while telehealth focuses exclusively on remote diagnosis and treatment. Our healthcare software development services help hospitals, clinics, and medical device companies create HIPAA-compliant platforms that reduce patient wait times, lower treatment costs, and improve chronic disease outcomes.

No matter how ‘emerging’ the virtual health trend seemed for the past decade or two, adoption of it hasn’t been massive. Now, the shift towards health system investment in virtual healthcare solutions is undeniable, driving demand for custom HealthTech development solutions.

In this blog post, we’ll explore the new horizon of telehealth and virtual health, and describe the difference between the two trends (to avoid confusion).

We’d also explore the forecasts of the leading consultants’ firms (such as McKinsey’and PwC) reports and takeaways on virtual health, and try to figure out the full potential of the trend in the modern healthcare tech world.

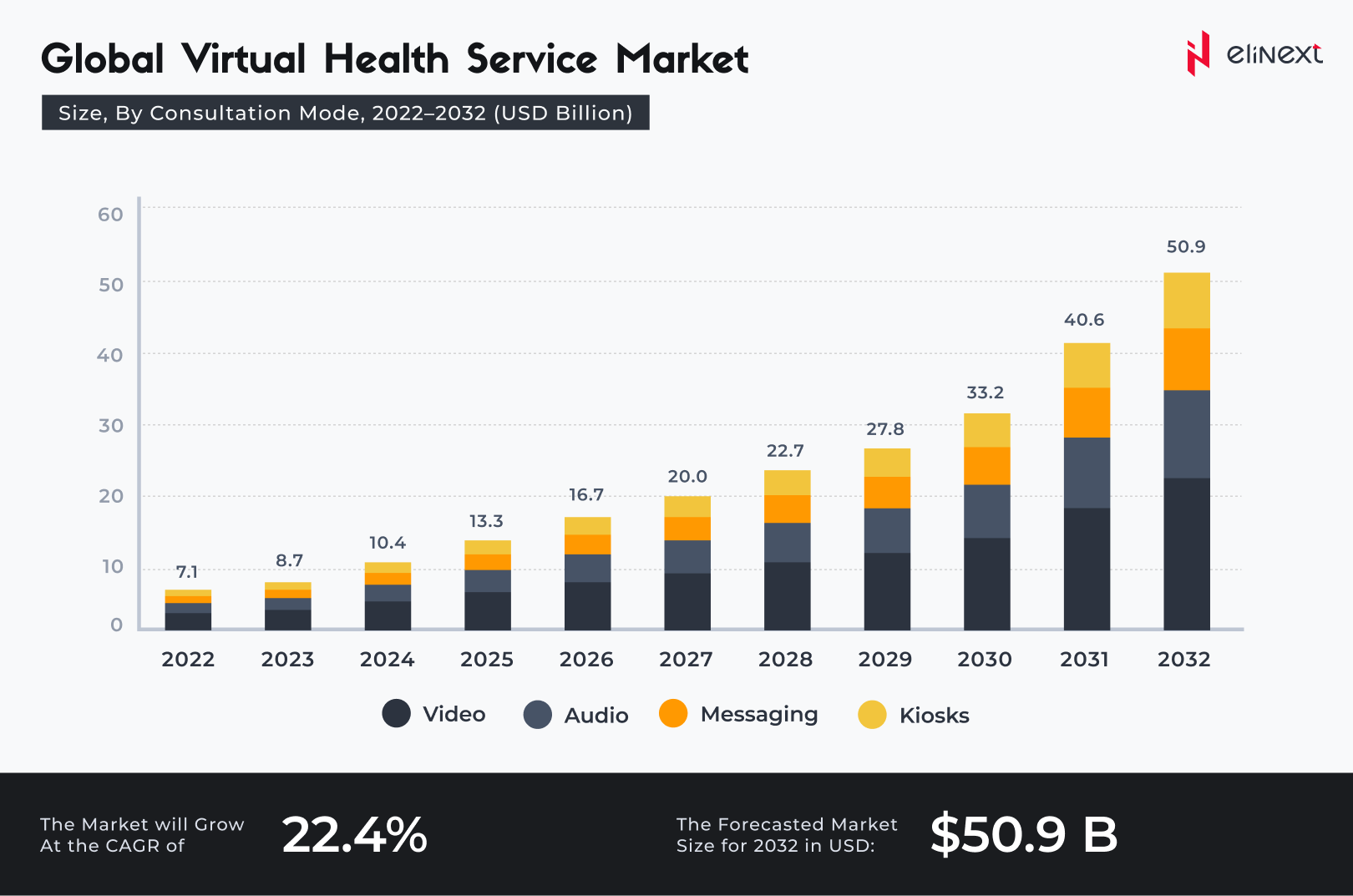

The global telemedicine market is projected to reach $151.08 billion in 2025. Virtual healthcare solutions integrate scheduling, remote monitoring, video consultations, and synchronization with electronic medical records. As a telemedicine app development company, we create systems that reduce no-shows and readmissions by up to 30%.

How Is Virtual Healthcare Different from Telehealth?

Virtual healthcare (aka remote patient management) is closely interlinked with telehealth, or telemedicine, but not interchangeable.

Virtual care is a broader term that defines the wholesome of remote tech-driven healthcare

Marcus Grindstaff, COO of Care Innovations, describes the entirety of terms for different distance healthcare operations in the following manner:

“Telehealth is a very broad category of solutions that service patients at a distance — so it could be doctor visits at a distance, it could be chronic condition management, it could be managing high-risk pregnancy. But doing that at a distance, doing it remotely.”

According to McKinsey’s report, the definitions in the area are the following:

That the terms are so often confused indicates how integral virtual health solutions are to telehealth delivery. Either way, demand is growing for a means to avoid the expense, burden and time spent traveling to and from clinics or doctor’s offices. And in rural areas struggling to attract physicians and practitioners at all, eliminating the need for transportation isn’t just a matter of convenience but also of basic access — especially for those unable to drive.

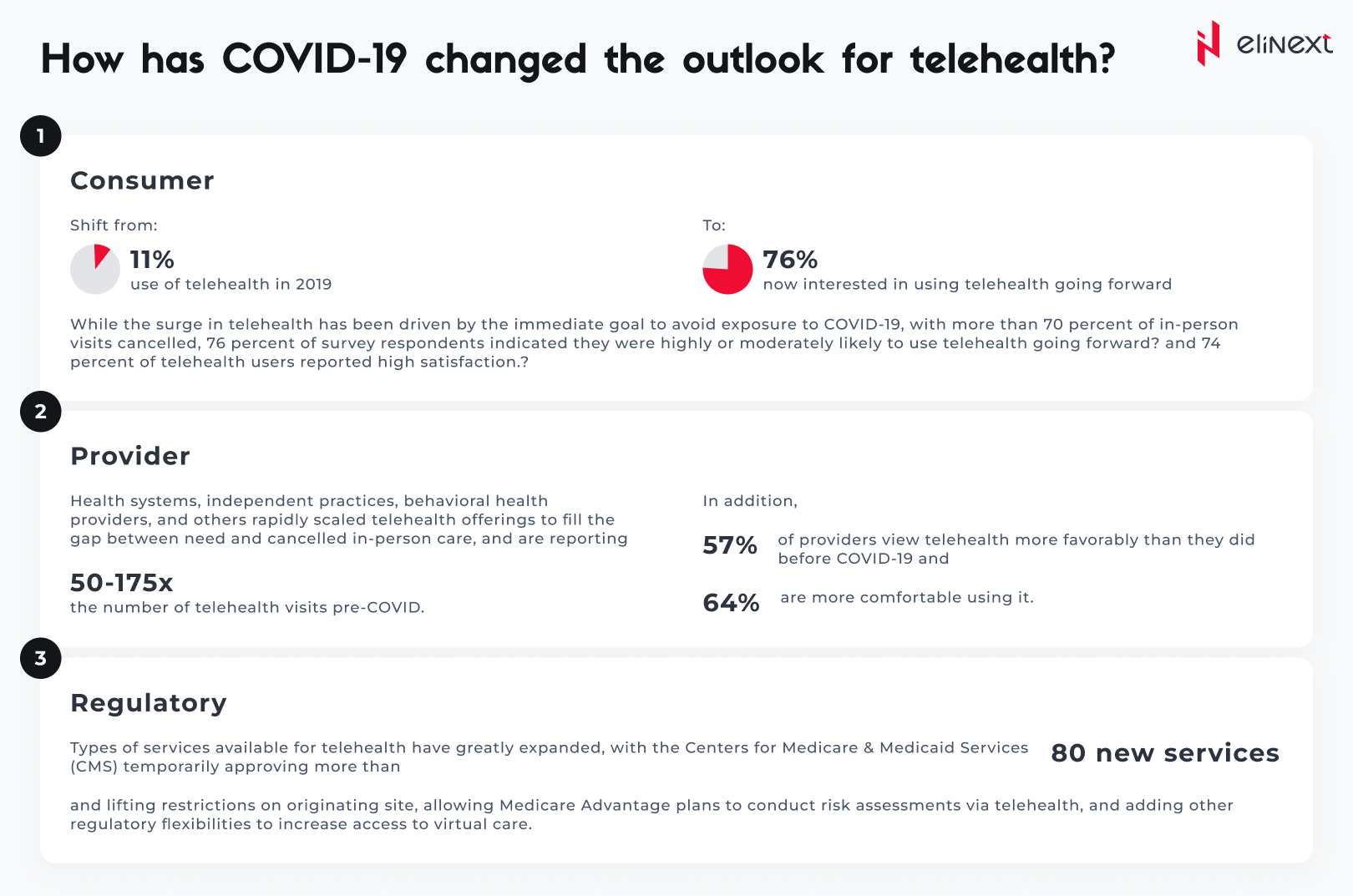

It’s also worth noting that patient demand for virtual healthcare solutions tends to transfer to satisfaction after implementation. Writing in the Harvard Business Review, Dr. Adam Licurse describes how a virtual visit pilot program at Brigham and Women’s Hospital yielded a 97% satisfaction rate among patients, with 74% stating “that the interaction actually improved their relationship with their provider.”

“We were encouraged to find that 87% of patients said they would have needed to come into the office to see a provider face to face if it weren’t for their virtual visit”, adds Dr. Licurse, who serves as the hospital’s Medical Director for Telehealth.Many of these dynamics are likely to be in place for at least the next 12 to 18 months, as concerns about COVID-19 remain until a vaccine is widely available. During this period, consumers’ preferences for care access will continue to evolve, and virtual health could become more deeply embedded in the care delivery system.

However, challenges remain. Our research indicates providers’ concerns about telehealth include security, workflow integration, effectiveness compared with in-person visits, and the future for reimbursement. Similarly, there is a gap between consumers’ interest in telehealth (76 percent) and actual usage (46 percent). Factors such as lack of awareness of telehealth offerings, education on types of care needs that could be met virtually, and understanding of insurance coverage are some of the drivers of this gap.

What is the full potential for telehealth and virtual care?

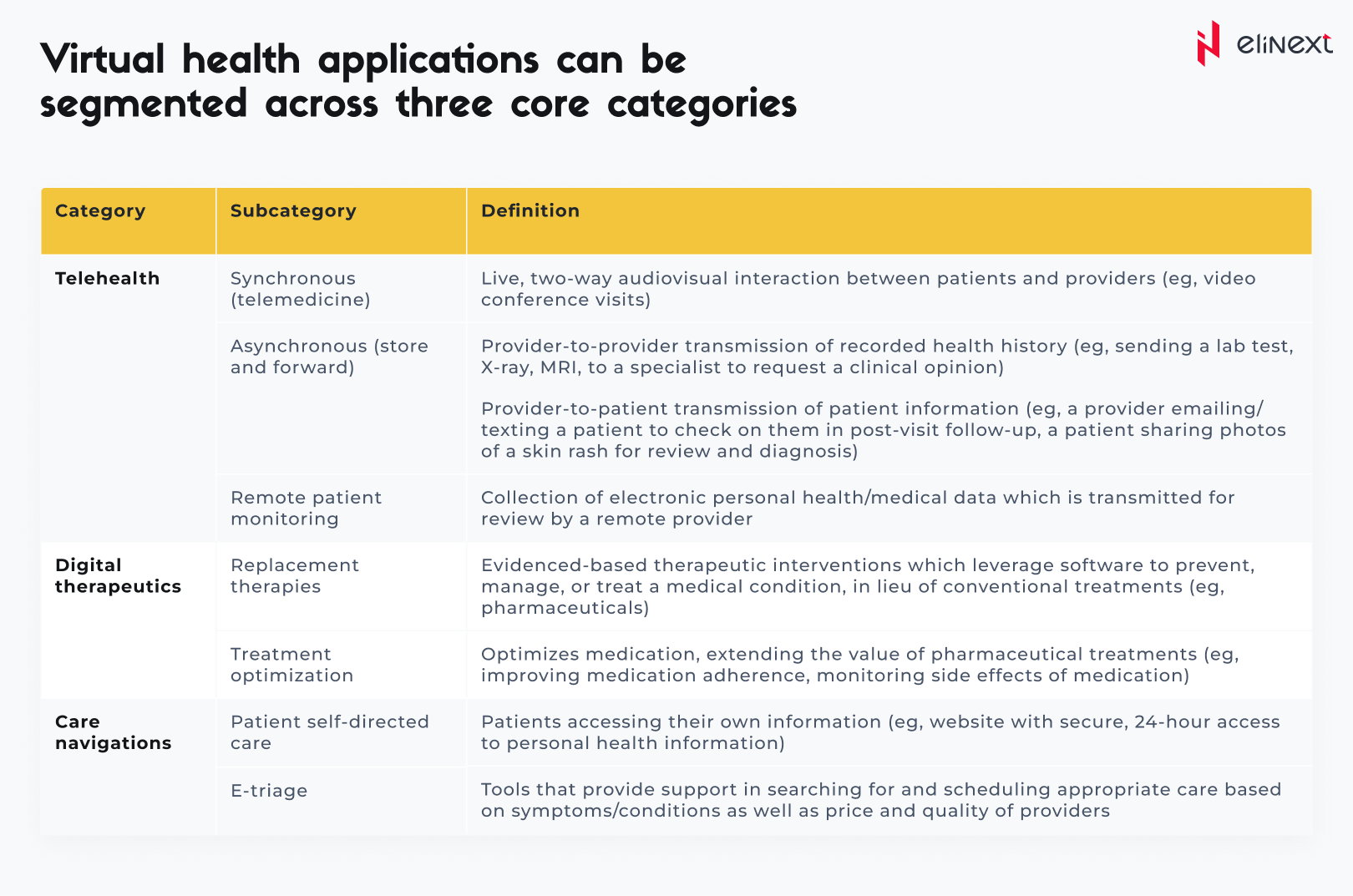

We identified five models for virtual or virtually enabled non-acute care and analyzed the full potential of healthcare volume and spend that could be delivered this way. These models of virtual care have increasing requirements to engage broader and broader portions of the healthcare delivery system, going from offering one-off urgent visits, to building omnichannel care models that deliver a large portion of office visits virtually or near virtually, to embedding virtual services in-home care models. They include:

On-demand virtual urgent care as an alternative to lower acuity emergency department (ED) visits, urgent care visits, and after-hours consultations. These care needs are the most common telehealth use cases today among payers. This allows a consumer to remotely consult on-demand with an unknown provider to address immediate concerns (such as acute sinusitis) and avoid a trip to the ED or an urgent care center. Such usage could be further scaled to address a larger portion of low acuity visits previously seen in EDs.

Virtual office visits with an established provider for consults that do not require physical exams or concurrent procedures. Such visits can be primary care (such as chronic condition checks, colds, minor skin conditions), behavioral health (such as virtual psychotherapy sessions), and some specialty care (select follow-up visits such as virtual cardiac rehabilitation). An omnichannel care model that fully leverages virtual visits includes a mix of telehealth and in-person care with a consistent set of providers, improving patient convenience, access, and continuity of care. This model also enables clinicians to better manage patients with chronic conditions, with the support of remote patient monitoring, digital therapeutics, and digital coaching, in addition to virtual visits.

Near-virtual office visits extend the opportunity for patients to conveniently access care outside a provider’s office, by combining virtual access to physician consults with “near home” sites for testing and immunizations, such as worksite clinics or retail clinics. For example, a virtual visit of a patient with flu symptoms could be followed up by a trip to a nearby retail clinic for the flu test, with a subsequent follow-up virtual check-in with the primary care physician to consult on follow-on care.

Virtual home health services leverage virtual visits, remote monitoring, and digital patient engagement tools to enable some of these services to be delivered remotely, such as a portion of an evaluation, patient and caregiver education, physical therapy, occupational therapy, and speech therapy. Direct services, such as wound care and assistance with daily living routines, would still occur in person, but virtual home health services could enhance the patient’s and caregiver’s experience, extend the reach of home health providers, and improve connectivity with the broader care team. For example, a physical therapist could conduct virtual sessions with elderly patients at their home to improve their strength, balance, and endurance, and to advise them on how to avoid physical hazards to reduce the risk of falls.

Tech-enabled home medication administration allows patients to shift receiving some infusible and injectable drugs from the clinic to the home. This shift can happen by leveraging remote monitoring to help manage patients and monitor symptoms, providing self-service tools for patient education (for example, training for self-administration), and providing telehealth oversight of staff (for example, an oncologist overseeing a nurse delivering chemotherapy to a patient at home and monitoring for side effects). This would be coupled with home delivery of the therapeutics.

Action Plan for Entrepreneurs in the Virtual Care Industry

What actions should healthcare stakeholders take in the near term to shape this opportunity?

Actions payers could consider:

Define a value-backed virtual health roadmap, taking a data-driven view to prioritize interventions that will improve outcomes for priority populations, and develop strategies to digitally enable end-to-care care journeys.

Optimize provider networks and accelerate value-based contracting to incentivize telehealth.

Define approaches (beyond the immediate COVID-19 response measures) to reimbursement and covered services, embed in contracting, and optimize networks and value-based models to include virtual health. Align incentives for using telehealth, particularly for chronic patients, with the shift to risk-based payment models.

Build virtual health into new product designs to meet changing consumer preferences and demand for lower-cost plans. This new design may include virtual-first networks, digital front-door features (for example, e-triage), seamless “plug and play” capabilities to offer innovative digital solutions, and benefit coverage for at-home diagnostic kits.

Integrate virtual health solutions into the care delivery approach. Given the significant disruptions to providers, payers are reassessing their role in care delivery—from ownership of care delivery assets, value-based contracting, or anything in between. Consider options in virtual health (for example, platforms, digital-first providers) as a critical element of this approach. Elinext’s analysis of netflix dominates the market is apple plus a threat examines how subscription video-on-demand platforms compete for viewer attention — covering feature differentiation, content licensing strategies, and the technical requirements that determine which platform delivers the best experience on connected devices.

Reinforce the technology and analytics foundation that will be required to achieve the full potential of virtual healthcare solutions.

Actions health systems could consider:

Accelerate development of an overall consumer-integrated “front door.” Consider what the integrated product will initially cover beyond what currently exists and integrate with what may have been put in place in response to COVID-19 (for example, e-triage, scheduling, clinic visits, record access).

Segment the patient populations (for example, with specific chronic disease) and specialties whose remote interactions could be scaled with home-based diagnostics and equipment.

Build the capabilities and incentives of the provider workforce to support virtual care (for example, workflow design, centralized scheduling, and continuing education); align benefit structure to drive adoption in line with the health system and/or physician practice economics.

Measure the value of virtual care by quantifying clinical outcomes, access improvement, and patient/provider satisfaction to drive advocacy and contracting for continued expanded coverage. Include the potential value from telehealth when contracting with payers for risk models to manage chronic patients.

Consider strategies and rationale to go beyond “telehealth”/clinic visit replacement to drive growth in new markets and populations and scale other applications (for example, teleICU, post-acute care integration).

Actions Investors, Health Services and Technology Firms Should Consider

Here is the list of actions healthcare-related companies and their investor should mind while dealing with business.

Develop scenarios on how virtual health solutions will evolve and when based on expected consumer preferences, reimbursement, CMS, and other regulations.

Assess impact across virtual health solution/service types, developing a view of the opportunity for each solution/service type, including expected consumer/provider adoption, impact (for example, to outcomes, experience, affordability), and reimbursement.

Develop potential options and define investment strategies based on the expected virtual health future (for example, combinations of existing players/platforms, linkages between in-person and virtual care offerings), and create sustainable value.

Identify the assets and capabilities to implement these options, including specific assets or capabilities to best enable the play, and business models that will deliver attractive returns.

Execute, execute, execute. The next normal will rapidly take hold, and those that can best anticipate its impact will create disproportionate value. Don’t underestimate the potential of network effects.

Many healthcare providers confuse telemedicine with remote healthcare and implement disparate virtual health solutions that miss crucial touchpoints from remote monitoring to patient portals. At Elinext, our patient portal software development services integrate these layers into a single, manageable platform. The result: providers reduce gaps in care, lower administrative costs, and see measurable ROI within the first year of implementation.

Elinext Medical Software Expert

Conclusion

Virtual health solutions are no longer optional; they are defining how modern healthcare is delivered. The global telemedicine market is expected to reach USD 151.08 billion in 2025, demonstrating a CAGR of 24.7%. Remote patient monitoring (RPM) software is growing at a CAGR of 34.9% and is expected to reach $65 billion by 2030. As a trusted EHR software development company, Elinext helps healthcare organizations build integrated, compliant platforms that integrate telemedicine, RPM, and EHR data, transforming disparate digital tools into measurable improvements in care.

Virtual Healthcare Solutions: Terms Explained

-

Telemedicine

Telemedicine is the remote delivery of clinical services — diagnosis, consultations, and treatment — via secure video or messaging, eliminating the need for in-person visits. Example: A patient consults with a cardiologist via video call from home.

-

Telehealth

Telemedicine is a broader category than remote telehealth, encompassing both remote clinical services and non-clinical support such as provider training, health education, and health management delivered through digital technologies.

-

Remote Patient Monitoring (RPM)

RPM uses FDA-regulated connected devices (e.g., glucose meters, blood pressure cuffs) to collect patient health data outside of a clinical setting and transmit it to physicians. Medicare covers RPM for both chronic and acute conditions.

-

EHR/EMR Integration

EHR/EMR integration connects digital patient health records across multiple care settings using standards such as HL7 FHIR, enabling seamless data exchange between virtual and in-person care teams, reducing duplicate analysis and gaps in care.

-

mHealth (Mobile Health)

mHealth is a healthcare and public health practice supported by mobile devices — smartphones, tablets, and wearables. It includes patient health apps, DMR apps for chronic disease management, and clinical decision support tools for physicians.

-

Virtual Care Platform

A virtual care platform is an integrated digital ecosystem for remote healthcare delivery, including patient portals, video consultation modules, AI-powered triage bots, electronic health record (EHR) connectors, appointment scheduling, and remote monitoring dashboards.

-

AI-Driven Diagnostics

AI-based diagnostics uses machine learning models to analyze medical images, lab results, and patient data to support triage and diagnosis. AI tools in radiology now achieve accuracy comparable to or exceeding that of trained specialists.

FAQ

What is virtual healthcare?

Virtual health solutions are digital ecosystems that enable remote healthcare delivery. They are used to connect patients and healthcare providers through telemedicine, remote patient monitoring, and mobile healthcare apps. Enterprises use them to efficiently scale access to healthcare.

What is telehealth?

Telehealth is the remote delivery of healthcare through digital technology. It is used for clinical visits, patient education, and healthcare professional training. Organizations use it to expand access to healthcare beyond physical healthcare facilities.

How is telehealth different from telemedicine?

Telemedicine encompasses only remote clinical diagnosis and treatment. Telemedicine is broader and it also includes non-clinical services such as education and public health. Healthcare providers use telemedicine as a common digital framework for healthcare delivery.

Can Telehealth replace in-person visits?

Telemedicine effectively replaces many routine and follow-up visits. It is used for chronic disease management, mental health care, and prescription refills. Healthcare providers use it to book in-person appointments for complex cases.

What devices are used in virtual healthcare?

Virtual health devices include video-enabled tablets, smartwatches, connected blood pressure cuffs, and glucometers. They are used to collect and transmit health data. Healthcare providers use them to remotely monitor patients in real time.

How does remote patient monitoring (RPM) fit in?

RPM is a core component of virtual healthcare, collecting biometric data through connected devices. It is used to manage chronic diseases and prevent hospitalizations. Healthcare professionals use it for continuous patient monitoring from anywhere.

How does AI support virtual healthcare?

AI supports virtual healthcare through bots for patient triage, diagnostic image analysis, and predictive alerts. It is used to prioritize cases and reduce diagnostic errors. Healthcare professionals use AI to improve decision-making speed and clinical accuracy.