In FinTech, the future almost never shows up loudly. It slips in through minor product tweaks, subtle regulatory changes, and tools that go from “interesting” to essential almost overnight. By 2026, the real winners will be the ones who understand where money, data, and trust truly meet.

Let’s dive into our picks for fintech industry trends 2026 without any filler buzzwords. Only real examples that will definitely shape the industry and set the pace for future-proof financial software development services.

Key Takeaways

- $37 billion in fintech investments is expected around the world by 2026, according to PWS

- $60 trillion is the projected total value of instant payment transactions in 2025, Juniper Research says

- $41.16 billion will the AI-driven fintech reach by 2030 (Grand View Research, AI in Fintech Report 2024)

Top 10 FinTech Trends for 2026

Fintech industry trends 2026 will feel quieter but far more decisive. What stands out now are patterns already proving their value under real traffic, real money, and real regulation.

Decentralized Banking

In 2026, decentralized banking software development services will feel more like a rail you reach for when the old ones slow you down. Banks will use on-chain settlement to move cross-border money in minutes, without waiting for cut-off times and extra middlemen. Smaller firms also pay global contractors in stablecoins to avoid FX swings. And in trade deals, smart contracts will run escrow, so funds are released once the right documents are verified. And regulators are getting on board because the upside is hard to ignore: lower costs, faster settlements, and better tracing.

Hyper-personalization

FinTech products are getting better at reading the room and reacting before things go sideways. They pull in transaction history, cash-flow patterns, and a few behavioral cues, then tune offers in real time. Credit lines can loosen after big sales, and repayment dates can slip when cash gets tight, so users don’t get hit with fees. Teams that ship this well tend to see stickier customers and fewer late payments as the product feels like it’s working with you. The key is transparency: every decision needs a clear “why,” an audit trail, and controls that keep it fair.

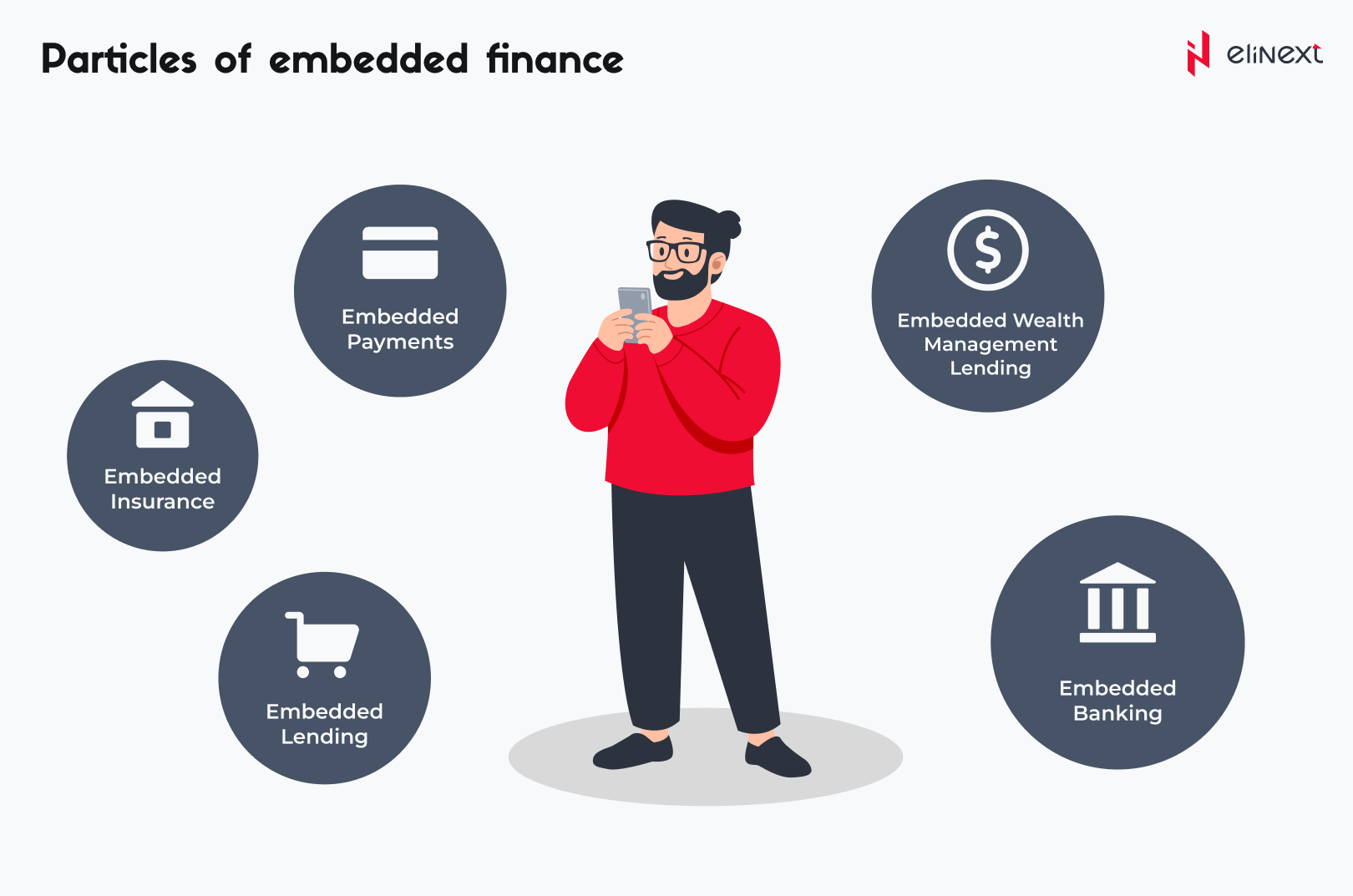

Embedded Finance Solutions

Among the latest trends in fintech, embedded finance turns platforms into financial hubs because it puts money tools right where users already work. A marketplace can offer instant seller financing based on real sales data, so vendors restock without chasing a bank. A SaaS dashboard handles payouts, taxes, and corporate cards in the same flow where banking teams invoice and reconcile. Once payments, credit, and spend management live inside the product, users stop jumping between apps, and churn drops drastically.

Digital Currencies and Tokenization

Banks use tokenized deposits to move large sums fast, but still keep the controls and reporting they already live by. Governments are testing CBDCs for benefits and tax payouts as money can land instantly, and the trail is easier to follow, which cuts fraud and “where did it go?” moments. Tokenization then takes the same idea and applies it to assets like bonds, invoices, and trade receivables, so ownership and settlement happen as a clean, trackable transfer. With assets that settle quickly and reliably, liquidity is freed up sooner, collateral moves faster, and capital gets put back to work.

AI Agents and Autonomous Finance

AI agents are creeping into finance the same way autopilot crept into planes: first as assistance, then as something teams truly rely on. They watch balances, spot patterns, forecast cash needs, and trigger actions that were previously manual – move funds, schedule payments, flag anomalies – based on rules you set. On the consumer side, agents can trim subscriptions, pick the best payment route at checkout, or warn you before a bill bounces. The make-or-break piece is governance: clear permissions, an audit trail for every step, and a “why” you can show to compliance.

Real-time Payments

Once payments go real-time, people stop tolerating “it’ll be there tomorrow.” Payroll can land in seconds, refunds hit while the customer is still on the checkout page, and cross-border transfers start to feel almost local. Rails like RTP and SEPA Instant prove that speed can scale without turning into chaos. That speed then seeps into product design: risk scoring happens live, and credit decisions are made while the transaction is still warm. The real shift is operational too, as cash positions update instantly, and reconciliation gets cleaner because the money simply shows up.

Super Applications

Money habits tend to bunch together, and super apps take advantage of that. You pay, you check your balance, move cash to savings, and you think about insurance, sometimes in the same hour. A super app strings those moments into one smooth flow inside a single interface, just like ERP for financial services. Because services share context, the experience gets smarter: spending insights can feed a savings plan, or a savings pattern can shape a credit offer. Platforms that pull this off see stronger engagement and higher retention as people share one endpoint to manage their financial lives.

AI-driven Compliance and Real-time Resilience

When everything moves faster, compliance can’t sit in a weekly report. It has to sit in the flow. AI-driven compliance, among financial technology industry trends 2026, monitors transactions, users, and system signals continuously, so unusual patterns get flagged while they’re happening. With better context, alerts become sharper too: fewer false positives, less “cry wolf,” and more time spent on real risk. The same setup boosts resilience since responses can kick in automatically before an incident snowballs into downtime.

Smarter Green Finance & ESG

Green finance is getting less “brand statement” and more about measurable math. Instead of vague ESG labels, platforms pull real data like energy use and tie it to specific transactions. That opens up practical products: a card program that shows carbon impact, or a loan that prices risk differently when sustainability data is verified. Tokenized carbon credits help, too, as issuance and retirement can be tracked end-to-end, with greenwashing harder to pull off. For banks and corporates, ESG shifts from a reporting headache to a signal you can actually invest around.

Financial Inclusion through Edge Innovation

Inclusion grows fastest when the product works in the real world, not just in good Wi-Fi. Lightweight apps run on cheap phones, offline payments go through and sync later, and agents act as cash-in/cash-out points when branches are far away. Risk scoring also gets more creative: instead of waiting for a credit history, lenders use alternative data like mobile patterns, merchant sales, and repayment behavior. That’s how credit gets priced for people who’ve never had a formal loan. When you design for patchy networks and everyday constraints, adoption follows because the product fits users’ lives.

Want to turn the latest trends in fintech into something you can actually ship?

Let’s map the fastest, safest path from idea to production with us.

“If I had to pick the fintech industry trends 2026, I’d keep my eyes on three things: real-time rails, AI software development companies pushing AI agents, and tokenization that lives inside bank-grade compliance. The hype will move on, but these are the shifts that change unit economics and user habits. And if you’re building embedded finance on top of them, you’re suddenly playing on hard mode – in a good way. By the way, Elinext can swiftly become your go-to choice for payment processing software development services.” – Anastasia Timoshenko, Fintech Consultant

Transform Your Business with Elinext FinTech Solutions

Elinext always stays in the loop of the latest trends in fintech and builds custom FinTech products end-to-end: mobile banking, digital payments (cryptocurrency wallet development services, mobile POS, gateways), biometric payment solutions, plus DeFi/blockchain apps and integrations. We add AI + analytics in fraud detection solutions for financial organizations, credit decisioning, and compliance automation with real-time monitoring. Need a team or turnkey delivery – we plug in fast.

The Future Trends in FinTech Industry

The fintech market trends 2026 keep evolving in small, practical steps that add up fast. Looking beyond today’s hotspots, a few quieter shifts are worth watching because they change how products are built and scaled:

- Open Finance 2.0: data sharing expands beyond bank accounts to include payroll, investments, telecom, and utility data. This creates a fuller financial picture, improving credit decisions, pricing, and personalization while keeping trust.

- Digital identity wallets: identity moves from one-off verification to reusable credentials. Users store verified KYC data and log in with passkeys, which cuts onboarding time, reduces fraud, and boosts conversion.

- Quantum-safe security: forward-looking teams begin upgrading encryption and key management now, protecting long-lived financial data from future “harvest now, decrypt later” threats.

FinTech success lives in the details most teams overlook.

Bring us your challenge, and we’ll help you turn it into a working solution.

Conclusion

Fintech market trends 2026 will feel less experimental and far more intentional. The products that win won’t chase trends – they’ll connect fast payments, smart automation, and trusted data into experiences people rely on daily. Our bet? The next leap comes from quiet integration: finance that adapts, protects, and scales without drawing attention to itself. When the tech fades into the background, that’s when it truly reshapes the industry.

FAQ

What are the most significant FinTech trends expected in 2026?

Real-time payments, embedded finance, AI-driven automation, tokenization, and smarter compliance will be among the most crucial fintech market trends 2026.

How will AI transform financial services by 2026?

AI will move from insights to action, automating risk checks, cash management, personalization, and compliance with clear guardrails.

Will traditional banks still be relevant?

Yes, but as platforms and partners. Banks that modernize infrastructure and collaborate with FinTechs will stay central.

How will payments evolve by 2026?

Payments will be instant, always-on, and context-aware, enabling live fraud checks, real-time credit, and faster reconciliation.

Is blockchain still relevant for FinTech?

Yes, especially behind the scenes. Tokenized deposits, settlement, and asset tracking deliver speed and transparency without user friction.

What cybersecurity threats should FinTechs expect?

More AI-driven fraud, account takeovers, and long-term data exposure risks, pushing teams toward real-time and quantum-safe defenses.

Will sustainability influence FinTech in 2026?

Absolutely. ESG data will affect pricing, risk models, and investment decisions, shifting sustainability from reporting to execution.

What opportunities should businesses prepare for?

Opportunities lie in embedded finance, automation, real-time data use, and building compliant infrastructure that scales fast.